From Counterparty Identification to Business Value: Using the LEI to Standardize the Extension of Commercial Credit

Facilitating the automation of all four phases of commercial credit processes

Author: Stephan Wolf

Date: 2018-01-17

Views:

A recent project undertaken by McKinsey & Company and the Global Legal Entity Identifier Foundation (GLEIF) identified three additional use cases for the use of the Legal Entity Identifier (LEI) relating to capital markets, commercial transactions and the extension of commercial credit. Whilst these are in no way exhaustive, they illustrate the broad application of LEIs. Our recent blog series includes the examination of the first two of these three use cases (see ‘related links’ below). This blog will therefore examine the use of the LEI in commercial credit.

When looking to extend credit to commercial borrowers, the first step for a lender is to ascertain the entity’s identity, history and ownership group-structure. This task is often much harder than expected. Many corporate groups and small businesses include numerous entities with similar names and each can then interact with the financial system in multiple ways, across multiple institutions and even in multiple countries.

This complex environment means that lenders – who often have siloed IT and data systems – may find it difficult to unambiguously identify unique customers. Sharing data within and across institutions to manage risk and exposure therefore becomes complicated.

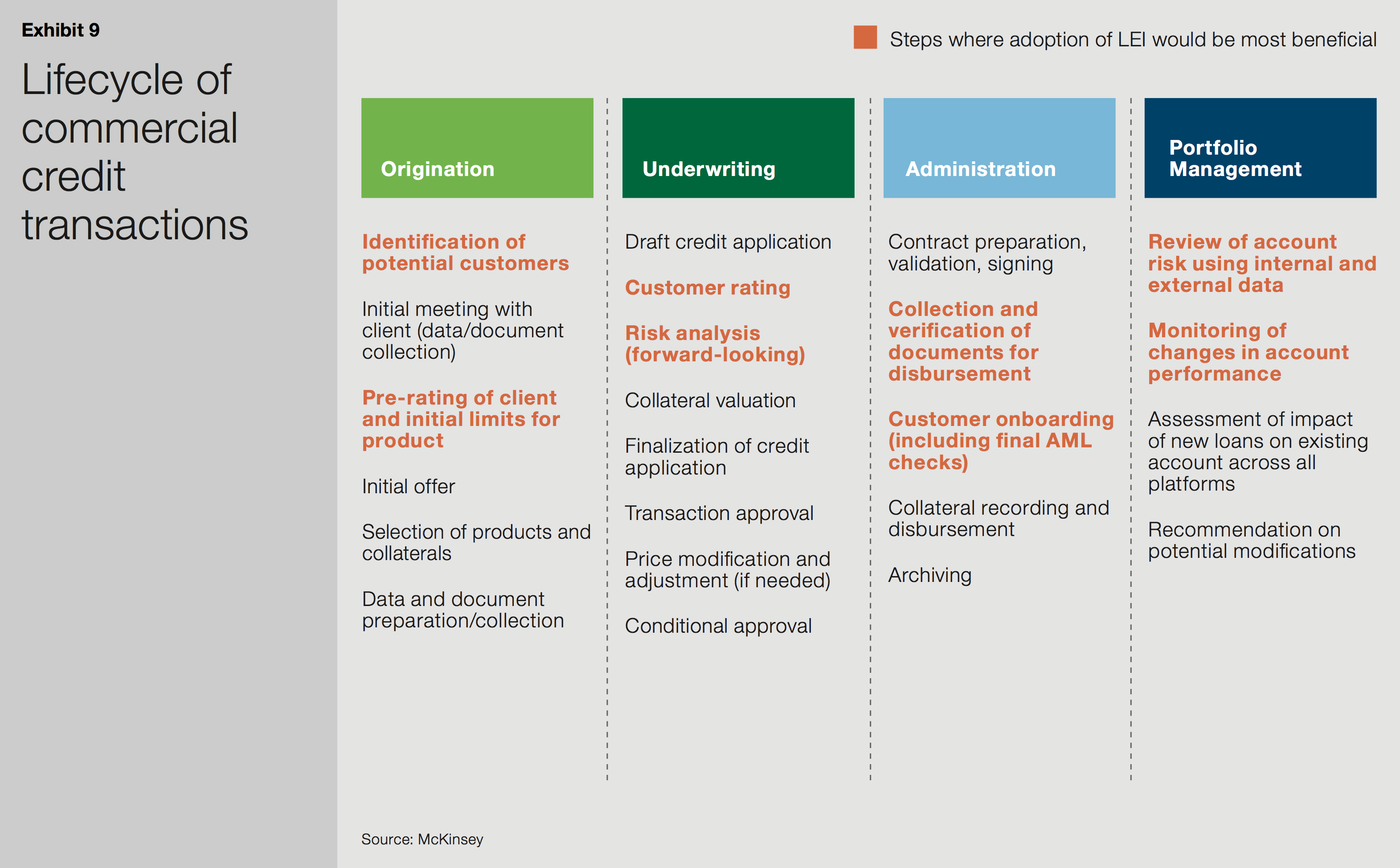

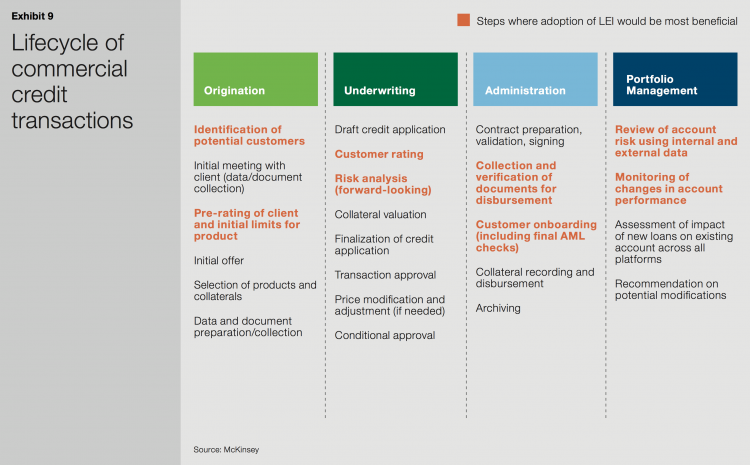

During each of the four key phases of the commercial credit lifecycle (origination, underwriting, administration and portfolio management), various checks are required which are often highly manual and time consuming. The use of the LEI allows for more robust and efficient know your customer (KYC) on borrowers as well as better traceability of information. All of which will yield considerable financial savings.

Graph from McKinsey & Company and GLEIF white paper titled ‘The Legal Entity Identifier: The Value of the Unique Counterparty ID'

Origination:

Having correct, verifiable information about the entity’s identity, history with the bank, and external financial/lending history is crucial during the origination phase. Without this information, it is almost impossible to offer appropriate products or assess risk accurately.

Human error is high in application forms with many entities failing to enter their complete name or entering a variation of the entity name previously used. This tendency is especially prevalent among small and medium sized businesses as well as affiliates of larger groups. The use of an LEI would help to standardize this vital information and as such, would significantly reduce the time that banks’ middle and back offices spend on manual verification processes.

Underwriting and administration:

The ability to easily and accurately trace an entity’s history is even more helpful during the underwriting phase, when final risk analyses and credit approval are undertaken. In addition, during the administration phase, when an entity is being onboarded to the lender’s systems, the use of a single identifier would strengthen and accelerate the required anti money laundering (AML) and compliance checks.

Portfolio management:

Finally, after the loan has been issued and the portfolio management phase begins, the lender must use internal and external data to review account risk while also monitoring changes in account performance. This requires a considerable amount of data reconciliation to ensure that the risk profile is up to date and accurate. LEIs could expedite data reconciliation and help to confirm its accuracy.

In all four phases of the commercial credit lifecycle, the use of an LEI would facilitate the automation and digitization of processes by providing a new data field that could be standardized across all systems.

Even beyond this, the McKinsey paper found that the three use cases – capital markets, commercial transactions and the extentsion of commercial credit – is by no means an exhaustive list. Introducing the LEI into almost any process that requires identification and verification of a counterparty – and that has a manual component – can deliver efficiencies and greater reliability.

As with any identifier, the broad application of the LEI highly depends on network effects within each industry subgroup, so we are encouraging not only the adoption of the LEI but also an open discussion about its various benefits amongst organizations in a wide range of sectors.

If you would like to comment on a blog post, please identify yourself with your first and last name. Your name will appear next to your comment. Email addresses will not be published. Please note that by accessing or contributing to the discussion board you agree to abide by the terms of the GLEIF Blogging Policy, so please read them carefully.

Stephan Wolf was the CEO of the Global Legal Entity Identifier Foundation (GLEIF) (2014 - 2024). Since March 2024, he has led the International Chamber of Commerce (ICC)’s Industry Advisory Board (IAB) of the Digital Standards Initiative, the global platform for digital trade standards alignment, adoption, and engagement. Before he was appointed as Chair, he had been serving as Vice-Chair of the IAB since 2023. In the same year, he was elected to the Board of the International Chamber of Commerce (ICC) Germany.

Between January 2017 and June 2020, Mr. Wolf was Co-convener of the International Organization for Standardization Technical Committee 68 FinTech Technical Advisory Group (ISO TC 68 FinTech TAG). In January 2017, Mr. Wolf was named one of the Top 100 Leaders in Identity by One World Identity. He has extensive experience in establishing data operations and global implementation strategies. He has led the advancement of key business and product development strategies throughout his career. Mr. Wolf co-founded IS Innovative Software GmbH in 1989 and served first as its managing director. He was later named spokesman of the executive board of its successor, IS.Teledata AG. This company ultimately became part of Interactive Data Corporation, where Mr. Wolf held the role of CTO. Mr. Wolf holds a university degree in business administration from J. W. Goethe University, Frankfurt am Main.

{kind=link}

{kind=link}

{kind=link}