Solutions

Featuring the LEI

LEI in Cross-Border Payments

Latest News:

GLEIF’s new eBook explains why the Legal Entity Identifier (LEI) should be an essential attribute of European Business Wallets (EBWs), especially for corporate treasurers and financial institutions operating in regulated financial ecosystems.

The publication demonstrates how embedding the LEI into EBWs strengthens trusted organizational identity and streamlines onboarding, payments, reporting, and compliance. By serving as a digital compliance layer within the wallet ecosystem, the LEI enables organizations to connect compliance requirements across financial services and facilitates more secure, interoperable, and scalable cross-border digital business transactions.

GLEIF’s new eBook explains why the Legal Entity Identifier (LEI) should be an essential attribute of European Business Wallets (EBWs), especially for corporate treasurers and financial institutions operating in regulated financial ecosystems.

The publication demonstrates how embedding the LEI into EBWs strengthens trusted organizational identity and streamlines onboarding, payments, reporting, and compliance. By serving as a digital compliance layer within the wallet ecosystem, the LEI enables organizations to connect compliance requirements across financial services and facilitates more secure, interoperable, and scalable cross-border digital business transactions.

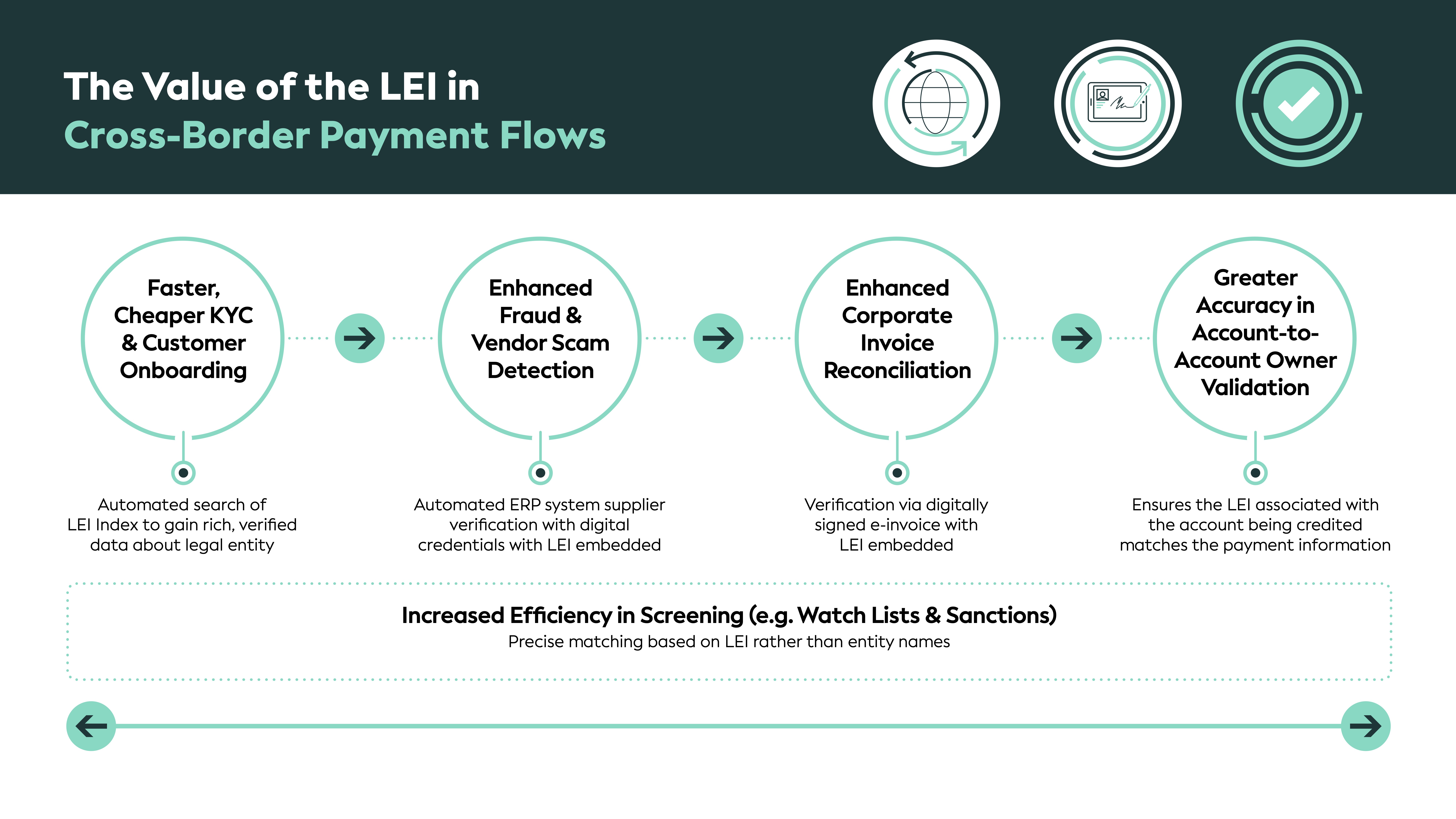

The LEI enables cross-border payment transactions to become faster, cheaper, more transparent, and more inclusive.

{kind=link}

When the LEI is added as a data attribute in payment messages, any originator or beneficiary legal entity can be precisely, instantly, and automatically identified across borders. As payment market infrastructures worldwide move to support instant payments, the ability to verify and validate the originator and beneficiary of a transaction in near real time is a foundational requirement to enable consumers, businesses, and financial institutions to confirm that funds are transferred across international borders to the correct entity.

The Financial Stability Board (FSB) has endorsed the LEI for supporting the goals of its G20-endorsed Roadmap for Enhancing Cross-Border Payments. As part of this initiative, and in collaboration with other industry standard-setting bodies, the FSB is currently working to promote standardized use in ISO 20022 payments messaging to mitigate constraints in cross-border payments. This includes the definition and harmonization of data fields - including identifiers - being transmitted along the payment chain.

GLEIF is working with leading stakeholders in the payments industry to demonstrate the significant value that the LEI brings to non-financial corporates and financial institutions when used in cross-border payment flows. The five key use cases are: screening; KYC and client onboarding; fraud detection and fight against vendor scams; e-invoice reconciliation; and account-to-account validation.

Read on to learn about these use cases and GLEIF’s pilot engagements:

The Value of the LEI: Cross-Border Payments Pilot Engagements

| Faster, Cheaper KYC & customer onboarding | Enhanced Fraud and Vendor Scam Detection & Corporate Invoice Reconciliation | Greater Accuracy Account-to- Account Owner Validation | Increased Efficiency in Screening (e.g. Watchlists & Sanctions) |

|---|---|---|---|