Onboarding Client Organizations: Impact of Complex Process on the Banking Sector

How financial services businesses can speed up KYC processes and work in a more streamlined fashion by adopting an LEI for each client organization

Author: Stephan Wolf

Date: 2018-06-12

Views:

In May 2018, the Global Legal Entity Identifier Foundation (GLEIF) published the report titled ‘A New Future for Legal Entity Identification’ which outlines the results of research that GLEIF recently undertook with research agency, Loudhouse, on the challenges of entity identification in financial services. The report also shows how replacing disjointed information with a globally accepted approach, based on broad adoption of the Legal Entity Identifier (LEI), would remove complexity from business transactions and deliver quantifiable value to financial services firms.

We summarized the main findings of the research, which surveyed over 100 senior salespeople in the banking sector in the UK, US and Germany, in a previous blog posted on 9 May 2018: ‘GLEIF Identifies That Over Half of Salespeople in Banking Spend 27% of Their Working Week Onboarding New Client Organizations’ (see ‘related links’ below).

This blog details the pitfalls of client onboarding identified with the research and explains how financial services businesses can save time, gain greater transparency and work in a more streamlined fashion by adopting an LEI for each client organization.

The report ‘A New Future for Legal Entity Identification’ as well as a separate document featuring the research findings are available for download on the GLEIF website (see ‘related links’ below).

The pitfalls of onboarding

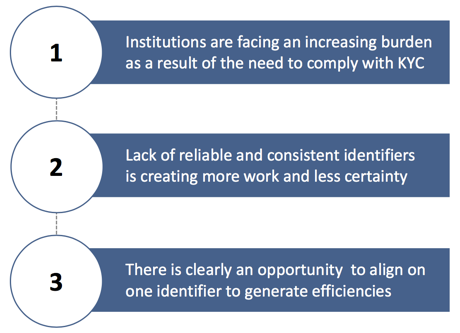

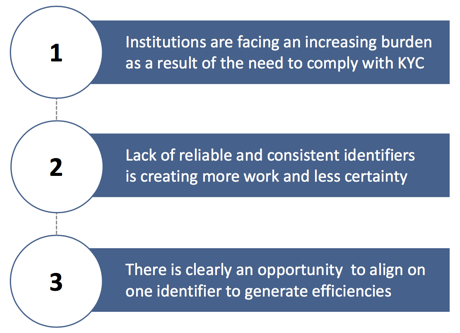

GLEIF’s research on the challenges of entity identification in financial services, including know your customer (KYC) due diligence, revealed that the process used to date for the onboarding of new legal entities is characterized by inefficiencies for many businesses in the banking sector. The research found that 50% of financial institutions use, on average, four identifiers to help identify client organizations.

In reality, what does this mean for senior salespeople, what is the impact on the broader business, and what can be done to improve the situation?

Principal challenges of onboarding client organizations

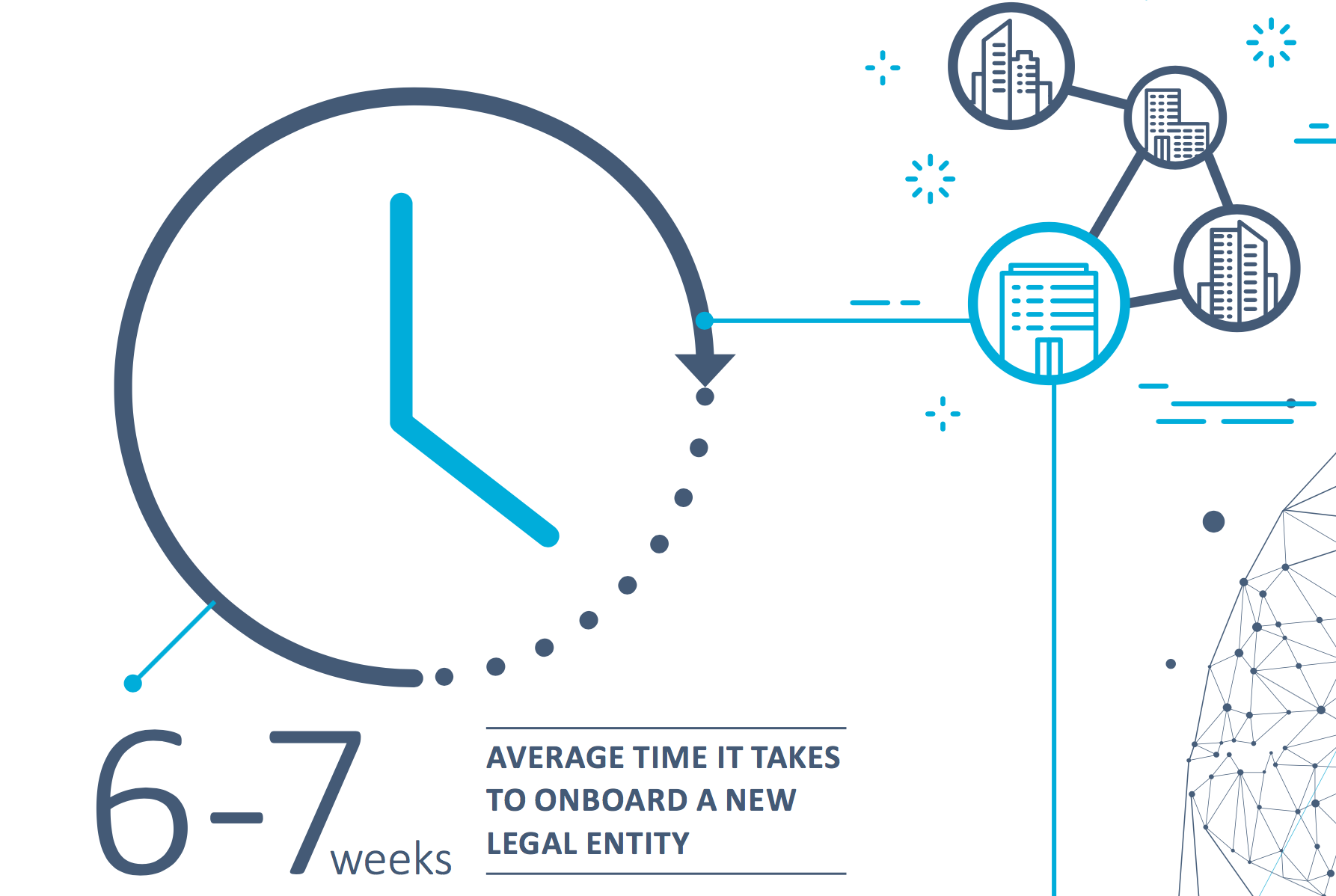

There is a clear consensus around the kind of challenges businesses are facing when it comes to the quality of the identifiers they are using – the same themes of reliability, contradiction and time come up again and again. 49% of survey respondents say that middle-and back-office activities related to onboarding are a major burden. What’s more, 57% of senior salespeople spend more than 1.5 days per week on tasks related to onboarding. As a result, it takes an average of six weeks to onboard a new legal entity (seven weeks, if more than four identifiers are used). Respondents, however, were not so clear on what was taking up their time. Some identify compliance with KYC due diligence (18%) as their biggest time drain, while others highlighted documentation management (16%) or identification of the legal entity (15%).

Lack of transparency and visibility impact risk management

These factors are having a considerable impact on the broader business. The issues associated with multiple identifiers include: inconsistent information; complex processes; a drain on resources; and a distinct lack of transparency. 46% of respondents acknowledge that the lack of transparency when identifying and reporting corporate structure does not bode well when it comes to meeting compliance regulations in financial institutions. Muddied waters make it difficult to evaluate risks properly meaning that onboarding and transacting decisions cannot be made with confidence, visibility or control. Ultimately, this means that both individual businesses and the industry as a whole are more susceptible to fraud and market abuse.

Length and complexity of the onboarding process impact business prospects

As well as draining time and hindering transparency, there is an even bigger business issue at stake. The research found that client organizations are not always sympathetic to the demands placed on financial services businesses by compliance regulations. Half of respondents (50%) agree that it’s becoming increasingly difficult to comply with KYC regulations. The top challenges identified include: the risk of losing business due to the length/complexity of the onboarding process (39%); client security concerns regarding who is able to access and view their documents (38%); and continuous changes in KYC regulation (37%).

This lack of sympathy means that client organizations are willing to move their business elsewhere if they feel that the onboarding process is taking too long. Lost business is highlighted as a very real consequence of the process, either through inability to glean adequate information or simply lack of patience on the part of the new legal entity. The research respondents believe that 15% of business is at risk as a result of the client losing patience with the process and 14% is lost because the client identity cannot be verified. The irony being, of course, that the legal entity might not find the process to be any quicker if they do take their business elsewhere – the research shows that the majority of financial institutions are all using four or more identifiers to onboard new entities and are therefore liable to the same inefficiencies.

How the LEI can help to improve the process

So, what can be done to improve the process – reduce the time taken, increase transparency and ultimately cut the amount of lost business? The fact that 52% of respondents believe the time to onboard will increase over the next 12 months means there is a clear opportunity to align on one identifier to generate efficiencies.

Banks operate in multiple jurisdictions and therefore need a global standard. The LEI offers businesses a standardized, one stop approach to entity verification.

Financial services businesses can gain greater transparency and work in a more streamlined fashion by adopting an LEI for each client organization. The roll-out of LEIs could also increase the stability of international financial markets and support higher quality and accuracy of financial data overall. But businesses could reap individual benefits too, including slicker onboarding, reduced inconsistency, less risk of business losses and more efficient use of valuable resources.

Replacing disjointed information with a globally accepted approach, based on broad adoption of the LEI, would remove complexity from business transactions and deliver quantifiable value to financial services firms.

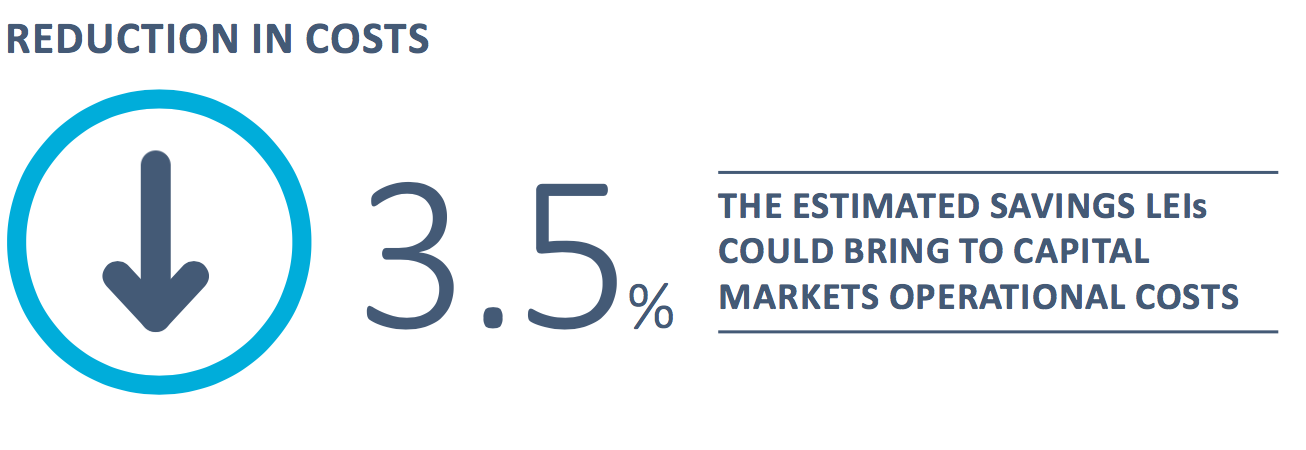

As has been demonstrated with a joint white paper by McKinsey & Company and GLEIF titled ‘The Legal Entity Identifier: The Value of the Unique Counterparty ID’ (see ‘related links’ below), introducing LEIs into capital market onboarding and securities trade processing could reduce annual trade processing and onboarding costs by 10 percent. This would lead to a 3.5 percent reduction in overall capital markets operations costs, amounting to over U.S.$150 million in annual savings for the global investment banking industry alone.

Significant amounts of time and money are lost by too many businesses, especially in the financial services industry, every time they make a business transaction as a result of a range of inefficient processes. This could be history for those businesses that adopt LEIs for their clients.

For more information, please read the full report titled ‘A New Future for Legal Entity Identification’, which details the results of GLEIF’s research into client identification in financial services and is available for download below.

Make sure you also keep an eye out for our next blog which will analyze the findings of our research on how the rise of digital technology in legal entity identification impacts client onboarding.

If you would like to comment on a blog post, please identify yourself with your first and last name. Your name will appear next to your comment. Email addresses will not be published. Please note that by accessing or contributing to the discussion board you agree to abide by the terms of the GLEIF Blogging Policy, so please read them carefully.

Stephan Wolf was the CEO of the Global Legal Entity Identifier Foundation (GLEIF) (2014 - 2024). Since March 2024, he has led the International Chamber of Commerce (ICC)’s Industry Advisory Board (IAB) of the Digital Standards Initiative, the global platform for digital trade standards alignment, adoption, and engagement. Before he was appointed as Chair, he had been serving as Vice-Chair of the IAB since 2023. In the same year, he was elected to the Board of the International Chamber of Commerce (ICC) Germany.

Between January 2017 and June 2020, Mr. Wolf was Co-convener of the International Organization for Standardization Technical Committee 68 FinTech Technical Advisory Group (ISO TC 68 FinTech TAG). In January 2017, Mr. Wolf was named one of the Top 100 Leaders in Identity by One World Identity. He has extensive experience in establishing data operations and global implementation strategies. He has led the advancement of key business and product development strategies throughout his career. Mr. Wolf co-founded IS Innovative Software GmbH in 1989 and served first as its managing director. He was later named spokesman of the executive board of its successor, IS.Teledata AG. This company ultimately became part of Interactive Data Corporation, where Mr. Wolf held the role of CTO. Mr. Wolf holds a university degree in business administration from J. W. Goethe University, Frankfurt am Main.

{kind=link}

{kind=link}

{kind=link}

{kind=link}