#17 in the LEI Lightbulb Blog Series -The Value of the LEI in Cross-Border Payments: Enhancing Account-to-Account (A2A) Owner Validation

In this blog, GLEIF’s Head of Business Operations, Clare Rowley, shines a light on how the payments industry is deriving value from the LEI in cross-border payments by exploring the world of account-to-account (A2A) owner validation.

Author: Clare Rowley

Date: 2024-05-22

Views:

The need to harmonize cross-border trust services continues to grow in line with the ever-increasing volume of trade and commerce taking place globally across digital platforms. In this effort, the LEI can play a fundamental enabling role.

The Financial Stability Board (FSB) has already endorsed the LEI to support the goals of its G20-endorsed Roadmap for Enhancing Cross-Border Payments. To demonstrate the LEI's value when transmitted in cross-border payment flows, GLEIF has been working with leading payments industry stakeholders to explore a variety of key use cases, including corporate invoice reconciliation, KYC, and customer onboarding, A2A owner validation, and screening efficiency for watch lists and sanctions.

What is A2A owner validation and why is it important?

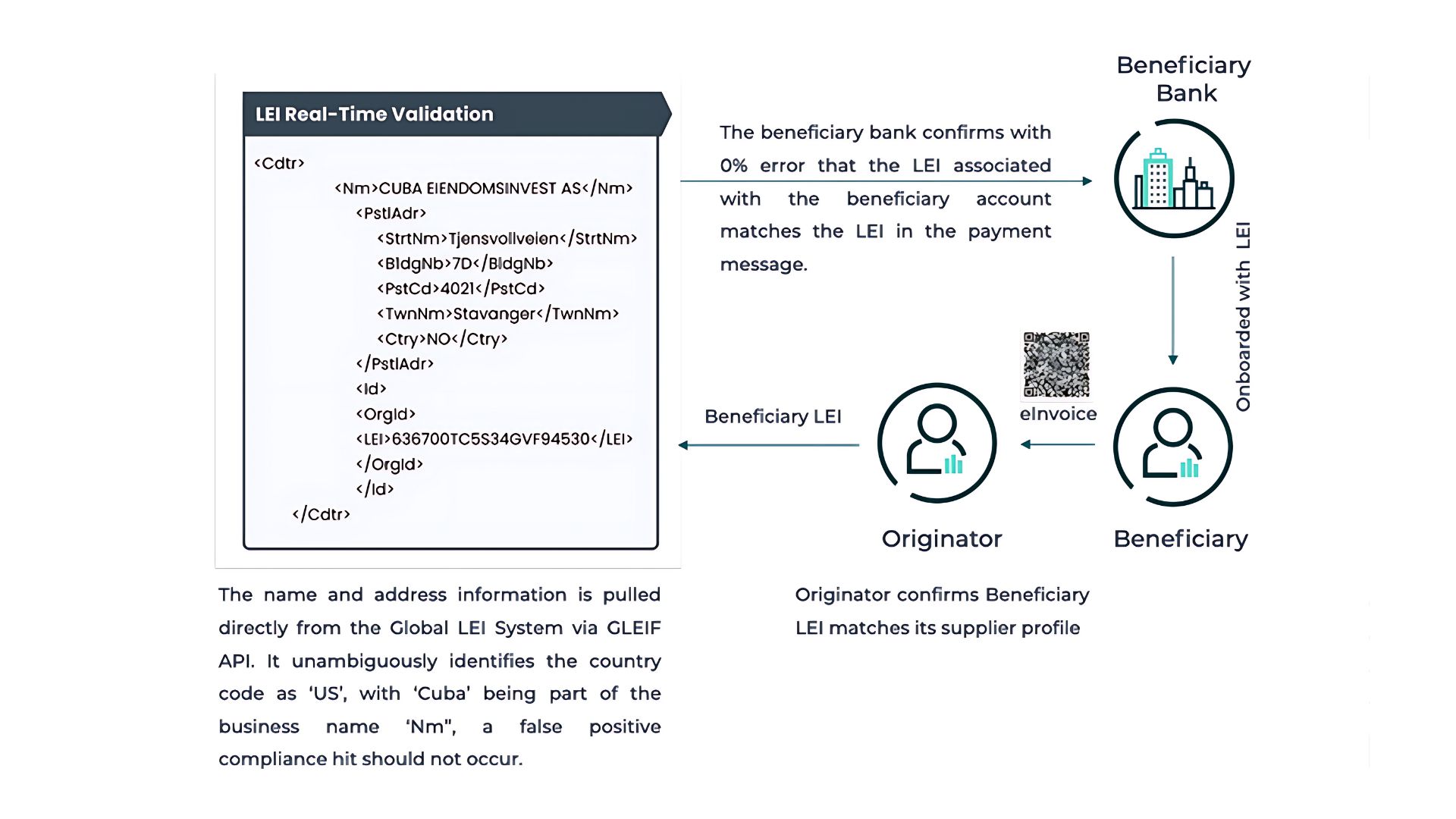

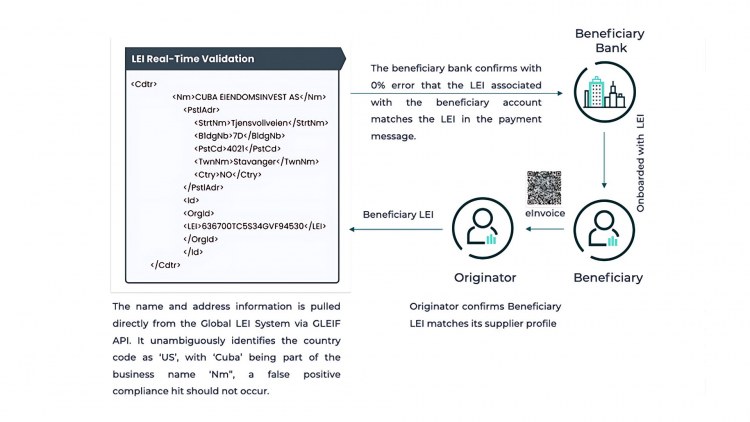

A2A owner validation ensures that a bank account belongs to the legal entity that claims to own it, enabling organizations to verify counterparties and originate payments.

A practical example of A2A validation in action is Pay.UK’s Confirmation of Payee service. Launched in 2020, this is an account name-checking service specific to domestic payments within the United Kingdom that helps to lower the rate of misdirected payments, providing confidence that payments are being sent to and collected from the intended account holder.

Understanding the core A2A challenge across borders

Despite some proven success on a domestic level, providing cross-border account validation services on either a regional or global basis will present significant challenges due to the varying possible implementations of structured ISO 20022 data at the domestic level, different languages and character sets, and local business identifiers.

Traditionally, names and addresses are used as a proxy for identity in payments, resulting in low match rates and the burden of the associated manual interventions required to investigate any discrepancies in account details by going back to the businesses executing the payments. Consequently, businesses trying to get on with their real work expend valuable resources chasing suppliers and navigating the specificities and complexities of local languages and addresses.

How can the LEI enhance A2A validation?

A single, global, digital identifier for legal entity beneficiaries across borders, legal jurisdictions, and payments schemes will allow for the development of effective cross-border confirmation of payee protocols. Happily, the LEI can play this role.

The Global LEI System is the only open and standardized legal entity identification system that has already been widely endorsed and mandated by financial regulators. Broad industry support stems from the fact that when the LEI is added as a data attribute in payment messages, any originator or beneficiary legal entity can be precisely, instantly, and automatically identified across borders and jurisdictions.

In Europe, the instant payments regulation already recognizes the LEI as a tool to facilitate international bank account number (IBAN) to account name matching. At a supranational level, the open FATF Recommendation 16 consultation suggests that beneficiary financial institutions should check that the beneficiary information in the payment message aligns with the information they hold. While the Recommendation 16 consultation does not directly reference the LEI in the confirmation of payee language, it references the LEI as an attribute for originators in beneficiaries, opening the door for the use of the LEI in the confirmation of payee.

The LEI contains the structured data of the entity’s legal name (in local language), translated or transliterated name, and address. This information can then be directly extracted from the Global LEI Index via GLEIF API calls, making it simple for banks to match the beneficiary information on the payment message with the beneficiary’s profile. Additionally, all major financial services data vendors have the LEI fully incorporated into their data products, allowing financial institutions to access the LEI data through existing commercial relationships. As a result, errors caused by incorrect/incomplete beneficiary names or addresses can be drastically reduced.

For example, corporates are often the target of fraudulent payments and must implement systems to reduce their impact. If the LEI is being used between corporates when signing a commercial contract or invoice, the originating entity could easily add the beneficiary entity’s LEI to the payment messages. The beneficiary bank could then validate the beneficiary’s LEI on the payment message against the one they have on file. This ensures that any fraud payment information with similar beneficiary name or account number information can be easily detected before the payment is credited.

Validating and updating LEI information, however, is key to ensuring compliance with regulatory requirements and mitigating the risk of fraud. Solutions such as Nucleus—from specialist payment consultancy Nth Exception—offer robust capabilities to address these considerations. By automating LEI validation processes, Nucleus helps financial institutions maintain accurate entity information, enhancing risk management in A2A payments:

The future of the LEI in cross-border payment flows

Simplifying and streamlining A2A validation is a clear demonstration of how the benefits of the LEI are being harnessed to enhance cross-border payment flows. Incorporating the LEI into cross-border account validation messaging can increase match rates, decrease validation responses, and limit the requirement for manual intervention. Ultimately, this will help to reduce misdirected payments and enhance fraud prevention, detection, and intelligence monitoring.

More broadly, there is growing industry recognition of the foundational role that the LEI can play in making cross-border payment transactions faster, cheaper, more transparent, and more inclusive—while maintaining their safety and security—in support of the G20 roadmap.

Robust implementation of the LEI in domestic payments systems is an important stepping stone towards unlocking the full potential of LEI for cross-border payments through strong and effective usage. This is supported by local banking systems and databases requiring LEIs for their current business clients. India is one country setting the pace in this regard, with the Reserve Bank of India (RBI) and regulated banks emphasizing recording the validated LEI against their business clients to enable more precise verification.

Promoting global LEI adoption

As noted by the consortium of Indian banks that participated in a pilot project investigating the utility of the LEI for A2A validation, implementing a single global identifier standard requires broad industry engagement across payments ecosystems. In practice, the appetite for such broad change is driven by regulatory obligation. This is the golden opportunity for market infrastructures around the world to facilitate effective cross-border confirmation of payee by supporting the inclusion of the LEI within ISO 20022 payment messages as described by the Bank for International Settlements' Committee on Payments and Market Infrastructures (CPMI) and The Wolfsberg Group.

Other participants in the payments ecosystem can also facilitate this implementation:

Corporates: when signing a commercial contract, the counterparty’s LEI should be requested to ensure precise identification of the organization it is doing business with. This LEI should be incorporated into the corporates' ERP system and invoicing protocols with the business partner.

Financial institutions: ensure all business clients are tagged with the LEI at the time of onboarding.

Increased trust and transparency across borders and jurisdictions also promise to address challenges that go beyond ‘just’ payments, such as bolstering the fight against global financial crime, simplifying complex and opaque supply chains, and supporting the digitalization of global trade.

If you would like to comment on a blog post, please identify yourself with your first and last name. Your name will appear next to your comment. Email addresses will not be published. Please note that by accessing or contributing to the discussion board you agree to abide by the terms of the GLEIF Blogging Policy, so please read them carefully.

Clare Rowley is the Head of Business Operations at the Global Legal Entity Identifier Foundation (GLEIF). Prior to working with GLEIF, Ms. Rowley worked at the United States Federal Deposit Insurance Corporation where she led technology initiatives improving bank resolution programs and contributed to research on subprime mortgages. Ms. Rowley is a CFA® charter holder and holds a MS in Predictive Analytics from Northwestern University.

{kind=link}

{kind=link}