#21 in the LEI Lightbulb Blog Series – The UK Makes the Case for the LEI in Digital Asset Markets

Support for the LEI within the UK Financial Conduct Authority's (FCA) proposal for a comprehensive regulatory framework for the crypto asset sector offers an important new regulatory precedent – outlining the crucial role that trusted organizational identity must play to promote transparency, interoperability, and trust in regulated digital asset markets globally.

Author: Alexandre Kech

Date: 2026-05-26

Views:

The UK Financial Conduct Authority (FCA) has taken a significant step toward establishing a comprehensive regulatory framework for crypto-asset activities – and, in doing so, has made a compelling case for the use of the Legal Entity Identifier (LEI).

By explicitly incorporating the LEI into its proposed rules for record-keeping, disclosures, and supervisory reporting, the FCA is moving beyond high-level policy discussions and demonstrating how standardized organizational identity can address longstanding challenges in complex, cross-border digital asset markets.

Advancing digital asset oversight

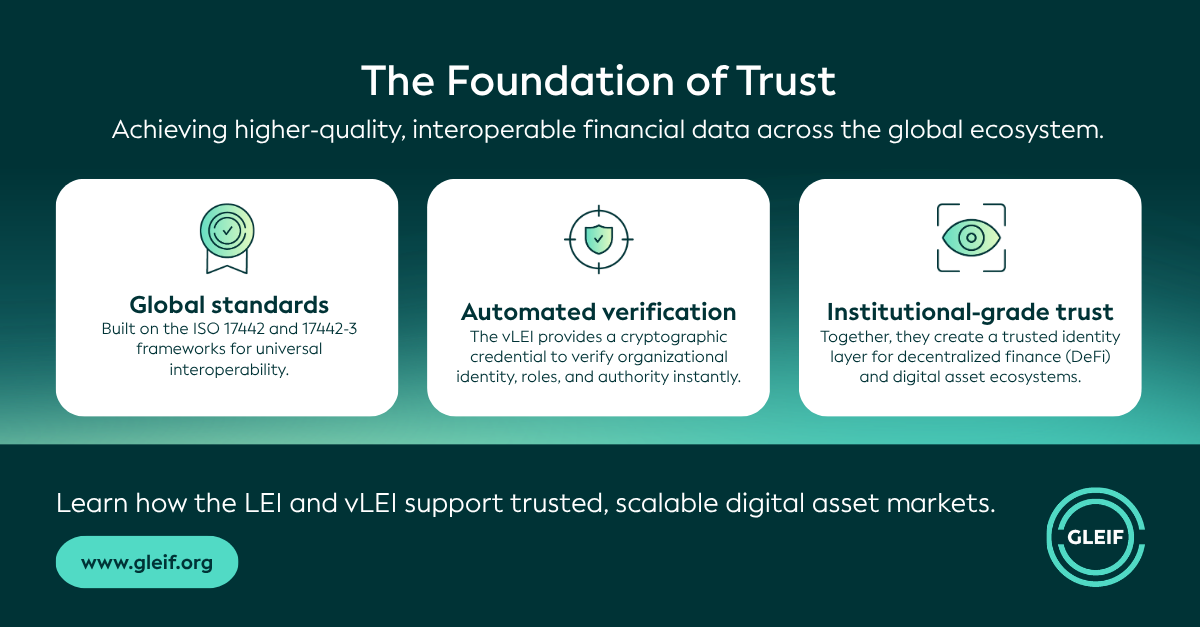

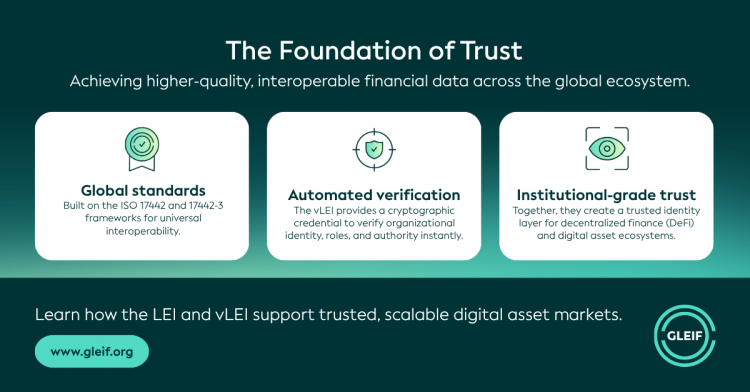

The need for increased trust and transparency across digital and crypto asset markets is driving increased regulatory momentum for the well-established Global LEI System as the only open, standardized, and regulator-endorsed organizational identity management infrastructure.

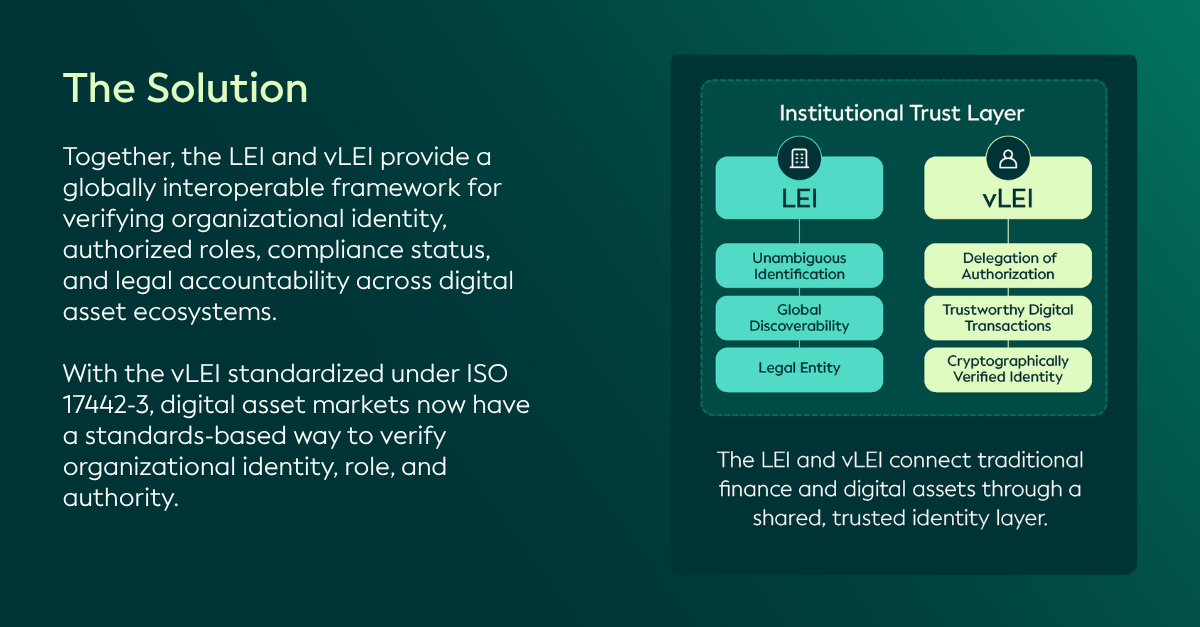

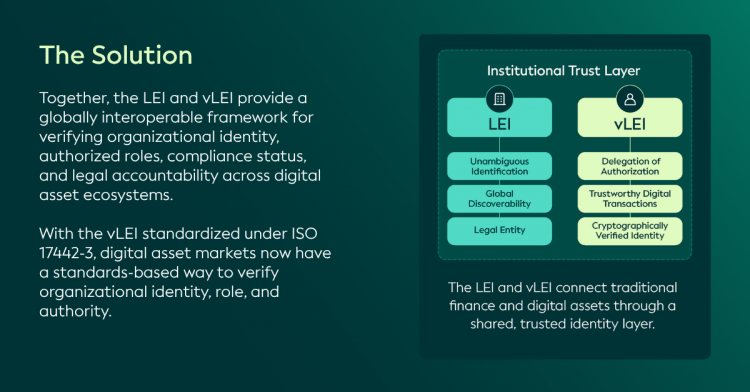

Through the LEI and its cryptographically verifiable counterpart, the verifiable LEI (vLEI), any legal entity can be uniquely and unambiguously identified – solving the significant problem of determining "who is who" across ecosystems and platforms. For regulators, this promotes interoperability, reduces fragmentation, and strengthens supervisory oversight – while lowering compliance costs and promoting innovation.

Previous editions in the LEI Lightbulb Blog Series have explored how these benefits are already recognized across regulatory frameworks, including the Financial Action Task Force's (FATF) updated Recommendation 16, which enhances payment transparency, and the European Union's landmark Markets in Crypto-Assets (MiCA) regulation. We have also examined emerging opportunities for the LEI and vLEI in relation to the GENIUS and CLARITY Acts in the United States.

This latest installment examines support for the LEI as part of the FCA's initiative to establish a comprehensive regulatory framework for crypto-asset activities.

Spotlight on the UK: FCA proposals on regulating crypto asset activities

To support the development of a competitive and sustainable crypto-asset sector that promotes market integrity, protects consumers, and supports innovation, the FCA has consulted on proposed rules and guidance for firms conducting regulated crypto-asset activities. These proposals have been informed by extensive engagement with the crypto asset industry, consumers, traditional finance participants, and other regulatory regimes.

The proposals mark an important step forward, moving beyond high-level policy and focusing on how crypto regulation will work in practice. Collectively, they demonstrate how clear, structured legal entity identification can address longstanding challenges by increasing transparency and reducing ambiguity in complex, cross-border crypto markets – enabling more effective, data-driven supervision.

As part of this, GLEIF welcomes and endorses the following FCA proposals requiring the use of the LEI for record-keeping, disclosures, and supervision. This reinforces its role as a proven, pragmatic, and scalable means of promoting transparency, interoperability, and trust in regulated digital asset markets:

CP25/40 – Regulating Crypto Asset Activities

Robust record-keeping of client orders and transactions is a key component of effective risk management and market integrity, especially in rapidly evolving crypto asset markets. In response to this need, the FCA proposes to require the use of unique digital identifiers, including the LEI, for sellers, buyers, or decision-makers involved in qualifying crypto asset transactions where these parties are legal entities.

CP25/41 – Admissions & Disclosures and Market Abuse Regime for Crypto Assets

The FCA proposes to require crypto asset trading platforms (CATPs) to file approved qualifying crypto-asset disclosure documents (QCDDs) – and any supplementary disclosure documents (SDDs) – with an FCA-owned centralized repository prior to the commencement of trading, and to publish these documents on their websites. These requirements are an important mechanism for ensuring transparency, market integrity, and consistent access to disclosure information. High-quality and reliable disclosures at the point of admission to trading are also essential for fair competition and the orderly functioning of crypto asset markets.

To support this need, the FCA proposes to require the use of unique digital identifiers, including the LEI, within QCDDs for qualifying stablecoin issuers, as well as for CATP operators submitting such documents in relation to legal persons seeking admission to trading.

Further to the FCA proposal, GLEIF observes that requiring vLEI signatures on QCDDs would enhance the reliability of disclosures and provide additional safeguards against fraud, thereby strengthening transparency and market integrity.

CP26/4 – Application of FCA Handbook for Regulated Crypto Assets II

Given that standardized regulatory reporting strengthens supervisory oversight of firms’ financial resilience, governance arrangements, and operational integrity, the FCA has proposed including the LEI in regulatory reporting, where available, or as an optional identifier.

Specifically, the consultation proposes the reporting of LEIs in several relevant contexts. This includes: for third parties involved in qualifying stablecoin issuance, backing, or redemption; the top 10 clients and/or execution venues of qualifying crypto asset trading platforms; intermediaries with the highest total transaction value of crypto assets; top liquidity sources when dealing in crypto assets as principal; and top lending counterparties.

Looking ahead, the vLEI could further strengthen transparency, security, and interoperability by allowing identity credentials to be embedded directly into digital transactions, smart contracts, and on-chain processes.

In addition to these proposals requiring the use of the LEI, GLEIF also encourages the FCA to support globally recognized identifiers like the LEI and vLEI in its proposed prudential disclosure framework:

CP25/42 - Prudential Regime for Crypto Assets

Proportionate prudential standards and transparent disclosures are key to supporting the development of the UK crypto asset market while maintaining market integrity, confidence, and resilience. The FCA’s proposals on the public disclosure of prudential information, including the introduction of a tailored disclosure framework for crypto asset firms and the inclusion of information on group arrangements, risk management, and own funds.

In this context, the LEI can support effective governance and strengthen the transparency and usability of publicly disclosed prudential information – particularly for cross-border group arrangements. Moreover, the vLEI could further enhance the reliability and auditability of prudential disclosures by enabling high-assurance, automated verification of disclosed information.

A growing regulatory consensus

The FCA proposals mark yet another compelling regulatory precedent highlighting the foundational role that the LEI, as well as the vLEI, can play in emerging regulatory frameworks to promote more trustworthy, resilient, and interoperable digital asset markets. This reflects similar developments in other jurisdictions, including the EU's MiCA regulation, which incorporates the use of the LEI to support transparency and consistent identification.

This builds on the long-established role for the LEI in traditional finance, where it is deeply embedded in major regulatory frameworks and industry processes. In EU and UK capital markets, the LEI supports entity identification across Markets in Financial Instruments Directive (MiFID II) / Markets in Financial Instruments Regulation (MiFIR) transaction reporting; European Market Infrastructure Regulation (EMIR) derivatives reporting; Securities Financing Transactions Regulation (SFTR) securities financing reporting; Central Securities Depository Regulation (CSDR); Market Abuse Regulation (MAR); Capital Requirements Regulation (CRR); Alternative Investment Fund Managers Directive (AIFMD); Solvency II; the Prospectus Regulation; and the Transparency Directive. This foundation is now being reinforced in the UK’s transition to T+1 settlement. The Accelerated Settlement Taskforce Technical Group, chaired by Andrew Douglas, identifies LEIs as a key data element for organizing counterparty reference data and recommends that onboarding firms record counterparties’ LEIs at onboarding, where possible.

As traditional finance evolves toward tokenized instruments and digital asset market infrastructure, consistent use of the LEI across both traditional and digital asset markets would enable smoother identity interoperability across platforms, ecosystems, and regulatory regimes, while the vLEI can add the cryptographic assurance, automated verification, and trusted delegation capabilities needed for digital asset markets to scale safely.

The proposals also highlight the broader potential of a systematic regulatory approach that extends the use of the LEI beyond traditional capital market applications, enabling any organization to be uniquely and unambiguously identified across borders, platforms, and systems. For instance, the FCA's new policy on Operational Incident and Third Party Reporting designates the LEI as the unique identifier for third-party reporting to help address risks and dependencies more effectively. This takes a similar approach to the EU's Digital Operational Resilience Act (DORA), which requires financial institutions to identify all EU-registered ICT service providers using an active LEI or European Unique Identifier (EUID), with the LEI mandated as the sole identifier for organizations registered outside the EU.

Together, these developments reflect growing regulatory and industry recognition of the LEI and vLEI as key enablers of the greater openness, accountability, and control now required across a data-driven, global digital marketplace. Ultimately, this will enable a more innovative and inclusive economy where trust is hardwired into every business relationship and interaction.

The ‘LEI Lightbulb Blog Series’ from GLEIF aims to shine a light on the breadth of acceptance and advocacy for the LEI across the public and private sectors, geographies, and use cases by highlighting which industry leaders, authorities, and organizations support the LEI and for what purpose.

If you would like to comment on a blog post, please identify yourself with your first and last name. Your name will appear next to your comment. Email addresses will not be published. Please note that by accessing or contributing to the discussion board you agree to abide by the terms of the GLEIF Blogging Policy, so please read them carefully.

Alexandre Kech is the CEO of the Global Legal Entity Identifier Foundation (GLEIF).

Prior to joining GLEIF, Alexandre Kech was Head of Digital Securities at the SIX Digital Exchange. As a member of the Executive Board, Alex had full executive responsibility for the Digital Securities business vertical, including sales and relationship management, product development, business design, and ecosystem expansion.

Over the past 25 years, Alex has constructed a unique career combining finance at BNY Mellon, payments/securities infrastructure and standards at SWIFT, and blockchain and digital assets at Onchain Custodian (ONC) and, most recently, Citi Ventures. As co-founder and CEO of ONC, Alex led the Singapore and Shanghai-based team that built custody and prime brokerage services for crypto and other digital assets from scratch. As Blockchain & Digital Asset director at Citi Ventures, he built a team to engage the European ecosystem on emerging use cases for blockchain technologies and digital assets.

Alex is also involved in industry and standardization initiatives. As the convenor of the ISO TC 68 / SC8 / WG3, which produced the ISO 24165 Digital Token Identifier (DTI), he is a member of the DTI Foundation Product Advisory Committee. He also recently served as co-chair of the Global Digital Finance (gdf.io) custody working group.

Alex earned a bachelor’s degree in translation and an Executive MBA from the Quantic School of Business and Technology while building Onchain Custodian, putting theory into practice in real-time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}